Technology real estate company Opendoor (NASDAQ:OPEN) will be announcing earnings results tomorrow after market hours. Here’s what to look for.

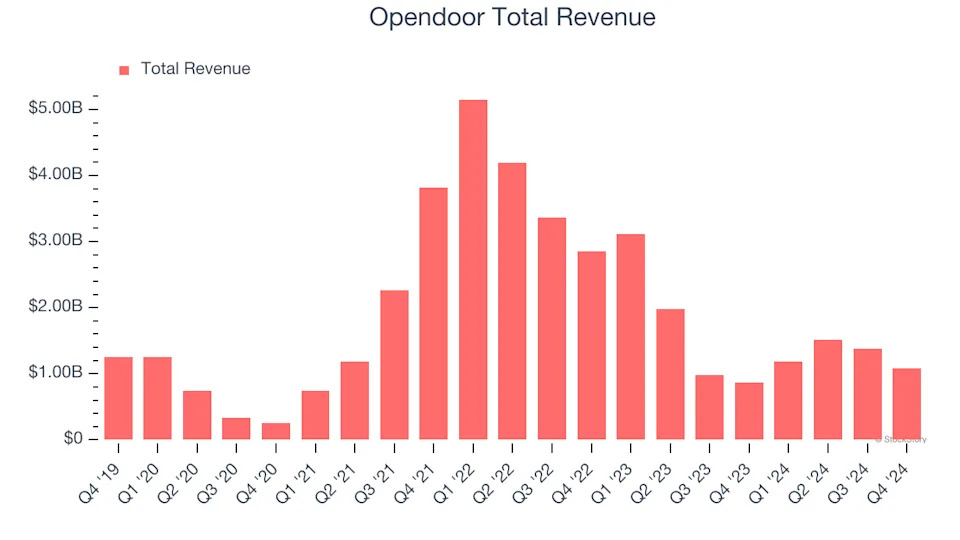

Opendoor beat analysts’ revenue expectations by 10.8% last quarter, reporting revenues of $1.08 billion, up 24.6% year on year. It was a satisfactory quarter for the company, with a solid beat of analysts’ EBITDA estimates. It reported 2,822 homes sold, up 19.4% year on year.

Is Opendoor a buy or sell going into earnings? Read our full analysis here, it’s free .

This quarter, analysts are expecting Opendoor’s revenue to decline 10.7% year on year to $1.05 billion, improving from the 62.1% decrease it recorded in the same quarter last year. Adjusted loss is expected to come in at -$0.10 per share.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. Opendoor has missed Wall Street’s revenue estimates three times over the last two years.

Looking at Opendoor’s peers in the real estate services segment, some have already reported their Q1 results, giving us a hint as to what we can expect. Cushman & Wakefield delivered year-on-year revenue growth of 4.6%, beating analysts’ expectations by 2.5%, and Newmark reported revenues up 21.8%, topping estimates by 8.9%. Cushman & Wakefield traded up 4.2% following the results while Newmark was down 2.5%.

Read our full analysis of Cushman & Wakefield’s results here and Newmark’s results here .

There has been positive sentiment among investors in the real estate services segment, with share prices up 8.8% on average over the last month. Opendoor is down 27.5% during the same time and is heading into earnings with an average analyst price target of $1.39 (compared to the current share price of $0.75).

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefiting from the rise of AI. .